Bridging loans have changed dramatically. Once seen as expensive emergency finance, they are now often one of the fastest, most flexible and most cost-effective ways to raise short-term funding — provided that they are arranged with the right lender, on the right terms.

Bridging loans have traditionally been associated with situations where a borrower needs to purchase a new property before the sale of their existing home has completed. This means the loan ‘bridges’ the gap between sending funds to buy and receiving funds later having sold.

Since property purchases usually involve substantial amounts of money, bridging loans tend to be relatively large sums, so opting to have one is always going to have a significant cost. This is why it is not a common practice to buy and sell homes using bridging loans, only when help is required to make the whole process easier.

Before the 2008 credit crunch, high street banks would provide bridging loans alongside other specialist products. However, following the crash, the banks withdrew most of their ‘specialist’ lending facilities to consolidate their activities, reduce overheads and focus on their main products, such as mortgages, overdrafts and bank loans.

This created a gap in the market, which led to the emergence of new specialist bridging lenders, who stepped in to fill it.

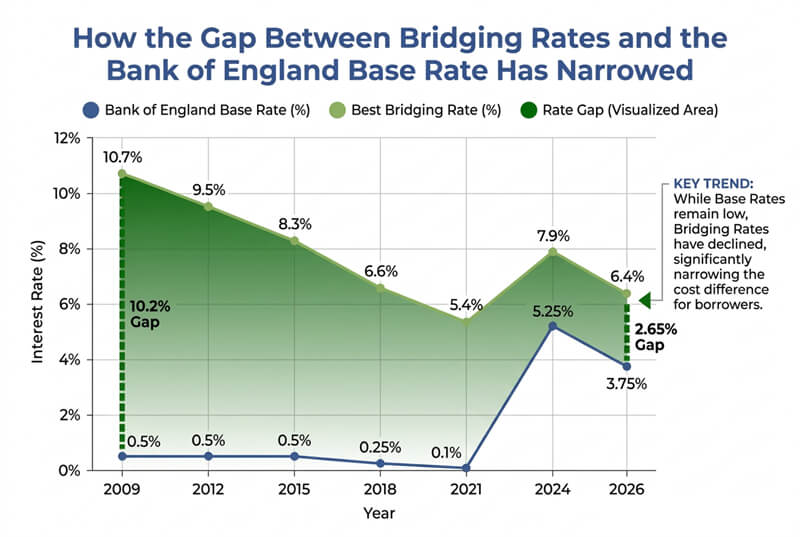

In March 2009 the Bank of England Base rate was only 0.5% pa and the ‘best priced’ bridging loans could be obtained from around 10.7% pa (0.89% per month). This made the difference between the Bank of England Base Rate, and the leading bridging rate 10.2% pa.

Since then, more new lenders have entered the bridging market, leading it to become dramatically more competitive. As a comparison, the 2009 ‘best priced’ bridging rates were more than 10% pa higher than the Bank of England base rate. Today that gap has fallen to around just 2.5% pa, highlighting how much the sector has matured.

GOOD - A large part of the bridging industry has evolved dramatically in recent years, with the difference between leading bridging loan rates and the Bank of England base rate shrinking significantly from around 10% per annum in 2009 to approximately 2.5% today. Therefore, bridging rates are now very competitive when compared to other low-cost methods of finance.

UGLY - The competitive and exciting side of bridging is unfortunately spoilt by a minority of bridging lenders in the market who damage the reputation of bridging through:

These lenders continue to fuel the belief among the critics that bridging is expensive and can easily cost borrowers huge amounts of money!

However, when structured properly, with the right lender, bridging loans are an enabler!

Whether a bridging loan is the best option will depend on how the funds are intended to be used and how it compares with other alternative forms of finance that may also be available for the borrower.

There are a number of situations where bridging finance stands out as being the best option, usually due to its speed, flexibility and cost-effectiveness.

Bridging loans can usually be secured against these properties, providing the funds to purchase, and if required, to also renovate the property. Upon completion clients will usually either sell the property, using some of the proceeds to clear the bridging loan, or, now the work is complete, refinance it using a standard mortgage.

Many properties purchased at auction are in a poor state of repair, making them unsuitable security for standard mortgages. These are the two main reasons why many auction purchases are funded using bridging finance.

In addition to the speed that bridging can provide, many bridging loans now have interest rates comparable to the cheapest forms of long-term finance, with the added advantage of no early redemption charges or exit fees. When buying with cash isn’t an option, bridging is therefore an ideal funding solution for this type of transaction.

Bridging loans have many uses but are not intended as a long-term finance option.

You need to have a good exit route, a reliable plan about how the loan is going to be repaid.

If your preferred exit plan is a little uncertain, then make sure you have a reliable back-up plan. In these circumstances make sure your back-up plan is progressed so that it is in place and ready to go if it is required.

Last updated: 05 May 2026 | © KIS Bridging Loans 2024 | Privacy Notice | Complaints Policy

We would like to hear from anyone who has had a bad experience, having taken out a bridging loan or an unregulated first charge loan.

For long term loans, this includes interest rate reductions not being passed on.

The more information that we have will help us better understand what borrowers are experiencing. Read More

All information shared with us will be treated as private and confidential and will not be shared with anyone outside of KIS Finance Limited.

Depending on the circumstances, we may also be able to offer guidance, comment on what has happened, or simply share our thoughts. If we believe we can help or advise you, we will let you know.

Any help that we do provide will be completely free of charge. Even if we help you achieve a better outcome or improved settlement, there will be no charge.

Please contact us if:

We are interested in knowing more about:

Borrowers with longer term loans – if you still have, or had, and old unregulated secured loan agreement taken out before the credit crunch in 2008, where the 13 year record low interest rates from 2009 to 2022 were not passed on. In other words if you had a loan that was not on a fixed rate taken out in 2008 or before, where the repayments or interest charges did not reduce despite the reduction in interest rates. Bank of England base rate was 5.25% in February 2008, 12 months later it was 1.0%, then dropped further, remaining under 1.0% for 13 years.

Contact us

Please use the form below or email ugly@kisfinance.co.uk in confidence, and tell us what happened and include as much detail as you can. Alternatively send your contact details and ask us to call you.