Is your current property taking too long to sell?

Do you want to buy a new property but haven't sold your current one?

If the answer is yes, a 'buy before you sell' bridging loan could be the answer.

This is a short term loan that is used by people who want to get on and buy a new house or flat before they have sold their current property.

The usual way to move house is to sell your existing property before, or at the same time as you purchase your new home. This means that you can then use the money you receive from the sale of your current home to fund the purchase of your new one.

Bridging loans can release equity and provide the funds required to complete the purchase of a new home before your current property has been sold.

You may want to get on and buy your new home before you have sold your current property for many different reasons.

“Buy before you sell - you want to buy a new property but haven't sold your current one.”

There are 2 main reasons:

If you want a no obligation, casual chat about how a bridging loan may help you, then please just call. Every member of our small and friendly team have considerable experience arranging bridging loans, and are always happy to help.

Calls are always answered by experienced advisors, 7 days a week (including Bank Holidays)

A small perk with having a bridging loan - you can move more gradually, as you don’t have to be out of your current property quickly, because you still own it. Our bridging clients often enjoy the time to look around their new empty property, decide on any work to do, or perhaps just decorating and taking a bit more time to get everything the way that they want it, before moving their belongings in.

Bridging loans make it possible to borrow money on a short-term basis by using the available equity in a property as security.

When a bridging loan is being used for a buy before you sell, it can be secured solely against the property being sold, alternatively just against the property being purchased, or it can also be secured against both properties.

Sometimes, when the borrower owns another property, such as a holiday home or a buy to let, these can also be used.

The preferred property to be used as security is usually the one being sold. However, when bridging loans are secured against more than one property, the next property used is usually the one being purchased. Other properties, including holiday homes and buy to lets, can also be used as security if required.

A bridging loan can be secured by way of a first charge or second charge, in the same way as a mortgage.

A first charge is used when there is no existing mortgage on the property, or when the bridging loan is being used to clear the existing mortgage, along with providing additional funds for the new purchase.

Usually if there is an existing mortgage this is left in place, so the bridging loan is secured as a second charge, behind the first charge mortgage.

Bridging loans are available up to 85% of a property’s current Open-Market-Value (OMV).

However, bridging plans above 75% are often unsuitable for ‘buy before you sell’ for the following reasons:

It is best to work to a maximum of 75% gross Loan-to-Value.

Gross LTV is the total amount of the loan facility. This includes 12 months of interest charges and the lender facility fee.

The net loan amount, takes off the interest and fees, so is the amount you actually receive from the facility. This can be easily calculated by using our Bridging Loan Calculator, which provides detailed interest charges and costings, or use our Maximum Net Loan Calculator below, which just calculates how much you can potentially borrow:

The lowest genuine interest rate currently available from the whole of the UK market is 0.55% per month. If you see lower advertised, it is most probably a gimmick, there are a lot of those around.

The best interest rates for bridging loans are available up to 50% LTV.

Once you go over 50% the rates start to increase, as higher LTVs are deemed a greater risk. Most lenders will have higher interest rates on their plans as their LTV bandings also increase.

The example below demonstrates bandings for our most popular plans. Here the interest rates increase quite gradually. The lowest rate here starts at 0.59%. Incidentally, the 0.55% plan has higher set up costs, which reflect in the overall cost, plus it is a plan that is harder to get accepted for.

| Loan To Value | Monthly Rate | Annual Rate |

|---|---|---|

| Up to 50% | 0.53% | 6.36% pa |

| 50% to 60% | 0.54% | 6.48% pa |

| 60% to 65% | 0.55% | 6.60% pa |

| 65% to 70% | 0.57% | 6.84% pa |

| 70% to 75% | 0.61% | 7.32% pa |

| 75% to 85% | 0.68% | 8.16% pa |

Please be aware that the more expensive lenders often have quite significant interest rate jumps between bandings.

Some lenders charge many more fees. To see a full list of fees and costs that different lenders may charge and why, please see bridging loan fees and costs.

Loan facility fee – This is generally 2% of the net loan amount.

For most loans we are able to reduce this facility fee, the amount by which depends on the amount being borrowed, and also on our arrangements with the lenders. For example: Fee table

Valuation fees – Our calculator provides an indication for the valuation cost if a physical valuation is required.

However, desktop valuations and AVMs are increasingly used these days, and if the security property, or properties, pass on these, there is no valuation fee for you to pay.

Obtaining a bridging loan requires solicitors to be involved. The bridging lender will have their solicitor and the borrower will also require a solicitor. The borrower is required to pay the legal costs for the lender as well as their own legal costs.

Some lenders offer a joint representation scheme, meaning you can use the same solicitor as the lender, for an additional cost of around £250. This option is usually a lot cheaper than instructing your own legal representative, plus it reduces delays by avoiding solicitors going back and forth to each other.

Our bridging calculator provides an estimate of the lender’s legal fees.

There is also the lender's admin fee, which is not paid upfront, only if the loan is taken out, along with the telegraphic transfer fee (to draw down the money). These can be added to the loan facility (they will incur some interest on them until the loan is repaid).

We have been providing bridging loans for over 16 years. Back then we made the decision not to charge any broker fees for advising and arranging bridging loans. We are today proud of the fact that our ‘No Broker Fee’ policy has remained in place throughout this time.

We also do not charge any administration or application fees!

How do we get paid?

The bridging lenders all pay commissions if a loan is taken out. The amount that the different lenders pay us does vary, and we are completely upfront about all commission payments.

Please use our bridging loan calculator to have a better understanding of the interest charges and the other costs associated with the bridging loan that you require.

There is quite a lot of information on this page, but here at KIS Finance we do like to Keep It Simple.

Please have a look at our bridging loan calculator which will give you an indication of the likely costs of having a bridging loan, including how much you will need to repay depending on how long you have the loan out for.

Please also remember that if you are buying a new home before selling your current one, you will need to allow for any ‘Additional Property Stamp Duty Surcharge’ as your purchase will count as an additional property. Provided you sell your current property within 3 years you can then claim the additional property surcharge element back from HMRC.

We have a useful Stamp Duty Calculator that you can use here.

Regulated bridging loans apply when property being used as security is residential and is the home of the borrower, or the home of any members of their immediate family. This can also apply if the security property is a former home of the borrower, or is intended to be the borrower's future home.

An unregulated bridging loan applies when the security property is used for investment purposes or as a business.

For example: buy to let properties, commercial property and land.

A regulated bridging loan provides much more protection to the borrower than an unregulated bridging loan does.

Read more about the differences between regulated and unregulated bridging loans.

If you are buying a new home for yourself before selling your existing home, then this is classed as a regulated bridging loan.

For most regulated bridging loans the loan term is set at 12 months with a 1 month minimum term.

Interest is calculated only up to the day that the loan is repaid.

There are no early redemption charges or exit fees.

Therefore, if you repay the loan after 3 months and 5 days, you will just be charged interest for 3 months and 5 days.

The only exception is if you clear the loan within the first month, because there is a 1 month minimum loan term. Therefore, if you clear the loan anytime within the first month, for example after just 1 week, you will be charged interest for the full month.

Interest is charged each month and is added to the loan balance. The borrower is not required to make monthly payments to pay the interest charged each month. Instead, it is paid at the end of the loan, when it is redeemed, so is included in the redemption figure.

Regulated bridging finance is arranged with a 12-month maximum term and a minimum term of 1 month. If you repay the loan during the first month, a whole month's interest will still be charged.

You can clear the loan before the end date without penalties. Interest is only charged up to the point the loan is redeemed. Interest is added to the original sum borrowed at the end of each month until the loan is repaid.

Unregulated bridging loans can have longer terms if required. This can be up to 24 months. Unregulated loan terms also vary, and so do the methods by which they calculate interest.

Please talk to us about the different options available.

Regulated bridging loans with terms over 12 months are available but are very limited.

There is one lender who will lend up to 24 months with interest rates that are very competitive.

However, for this loan there is an affordability check, as monthly interest payments need to be paid as there is no roll up option.

There is also an option for High Net Worth borrowers where the maximum loan term is increased to 60 months. Interest rates are also very competitive on this plan.

To qualify as High Net Worth and access these plans, you need to have either a total net income in excess of £300,000 per annum, or have total net assets in excess of £3 million.

For this type of loan, the security property, or properties, are usually either sold or refinanced.

If there is going to be a shortfall with the proceeds received from the sale of your property, and the amount required to clear the bridging loan, you need to consider how you are going to cover this.

For example, you may be planning to port your current mortgage to the new property, in which case it is important that you check with your current provider if this will be possible.

Or you may be planning to take out a new mortgage to cover the shortfall, in which case you need to make sure that you are in a position to get the required mortgage agreed, before taking out the bridging loan.

If you are over 55 you maybe considering taking out a lifetime mortgage to clear the bridging loan. Similar to taking out a mortgage, you need to ensure that this option is available to you, and that you will be able to raise sufficient funds to clear any shortfall.

If your exit strategy is something like an inheritance, sale of shares or a maturing investment, you may need to have a backup plan in case there is an unexpected problem or delay, meaning your planned exit doesn’t materialise.

Whatever your plans, you need to make sure that you have a good exit strategy in place, so that you are not left struggling to repay the bridging loan.

We also need to satisfy the lender that you will be able to repay the loan, using a method that they approve of.

It’s really simple to apply for a bridging loan with us.

Just give us a call and we’ll take some basic initial information, typically:

We will then get a loan facility approved for you and send you detailed terms, with a full explanation of all the costs involved - this usually takes about an hour.

We have access to all the UK’s best lenders, so taking into consideration your personal requirements and circumstances, you can be assured that you will be provided with the best interest rate and all-round deal that is available!

We can also provide confirmation to any estate agent or vendor that you:

This flexibility will help to get your offer accepted, plus can also help you secure a better deal on the purchase price.

Depending on the circumstances and how quickly you need the funds, application to completion can be achieved within 2 weeks.

For very urgent funding we have lenders who can do everything within as little as 48 hours, but this is dependent on certain factors.

It is better to allow a week for really urgent cases, as this will mean that you can still secure a very competitive deal.

We completely appreciate that bridging is often used as a back-up plan, in case something goes wrong with ‘Plan A’, you have a plan B.

If your Plan A, whatever it maybe, all works out, we understand that this is the best outcome for you. This actually happens a lot and is all part of the job for us.

There are also other occasions when it makes sense to change your mind about taking out a bridging loan. You may have doubts about your proposed plans, or there is an unexpected change in your circumstances. You have to be careful and do what is best for you and your family.

In the event that you need to cancel your bridging loan, KIS Finance do not charge any sort of cancellation fee, and this is also the case for the bridging lenders that we use.

Depending on how far your application has progressed, there may be some fees that you have already paid, for example a valuation fee and perhaps some legal fees.

These will only be for valuations and legal fees if they have been instructed. Payments for valuations would have either been paid directly to the company instructed to carry out the valuation, or to the lender. Legal fees are usually paid directly to the solicitor, or sometimes to the lender, who then pay the solicitor.

If a valuation fee has been paid, but the valuation has not yet been carried out, we maybe able to arrange a refund. We may also be able to arrange a full or part refund for legal fees, depending on if work has started, and if it has, how much has been carried out. Some legal fees are payable on drawdown of the bridging loan. If this is the case and the bridging loan is cancelled after legals have been instructed, the solicitor may send you a bill for any work that they have done.

Other costs such as the facility fee (lenders arrangement fee), administration fees and telegraphic transfer fee, will not be charged if the application is cancelled before the loan is drawn down.

The minimum age to take out a bridging loan is 18 years old, and there is no maximum.

Due to the short-term nature of this type of borrowing, some lenders do have an age limit whereas others do not.

The loan plans with the best deals are currently available for applicants who are between the ages of 21 and 85. However, there are some competitive plans available with no upper age restrictions.

Most bridging loans are arranged with the interest added to the facility each month or deferred until such time that the borrowing is repaid in full. As there are no monthly payments to make, affordability does not need to be assessed in the same way as most longer-term finance applications.

However, if your planned exit is refinance, then the lender will want to check that you have sufficient income to qualify for the long term facility that you are planning on taking out.

Although adverse credit does not on its own stand in the way of being able to obtain a bridging loan, your credit history is important when applying for a number of reasons:

It may affect the loan plan – the lenders who offer the best deals will only accept a very small amount of adverse credit history, and this needs to be quite historic.

Since bridging is only short term, are secured on property and not reliant on monthly payments, there are numerous bridging plans that still offer competitive interest rates whilst also accepting applicants who have Counts Court Judgements, defaults and mortgage arrears.

Credit history will need to be investigated more if you intend to refinance your bridging loan, as the lender will need to be satisfied that you will be able to meet the likely lending criteria required to arrange the proposed refinance facility. If the bridging loan is going to be repaid from the proceeds of a sale of a property, then having a poor credit history will not affect this.

However, if the plan is to exit by refinancing the bridging loan onto a longer term facility, a poor credit history can be an issue because the bridging lender will be concerned about your ability to secure a long term finance facility with a poor credit history.

The bridging lender needs to be satisfied that you have a viable exit plan that will repay their loan.

Many lenders will provide bridging finance for customers with adverse credit if they intend to repay the borrowing with money they will have readily available later, such as proceeds from selling a property.

We can secure loans on any type of property or land, often even un-mortgageable property and ones of non-standard construction.

The security property can also be in a very poor state of repair or in the process of being constructed.

If you have anything unusual, then please give us a call to discuss.

All the owners of any property used as security need to be included as named borrowers taking out the bridging loan.

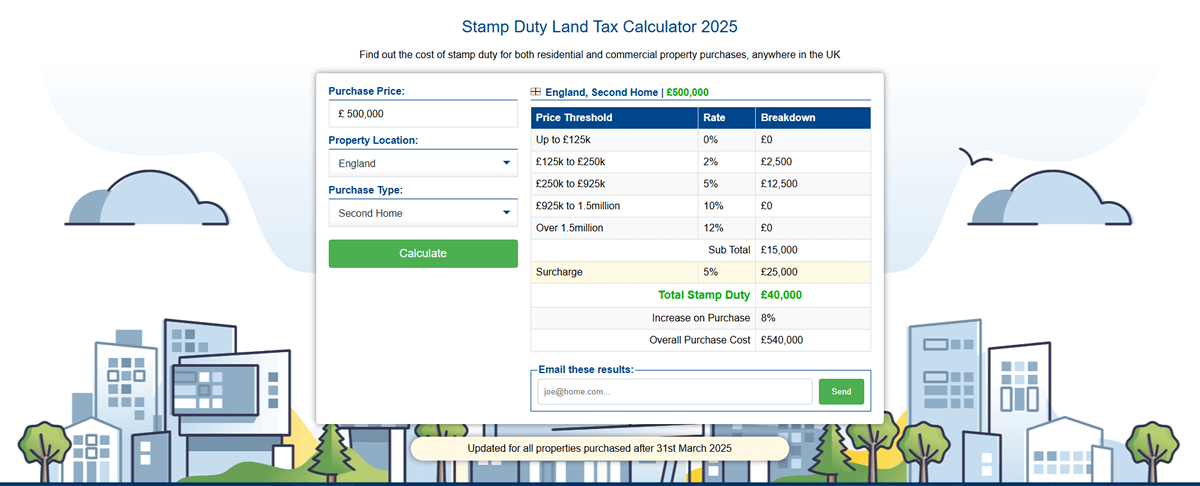

When you buy your new home, if you haven’t already sold your current home, this new property will be classed as a second home for stamp duty purposes. Therefore, in addition to the normal residential property stamp duty, you will also need to pay the extra second home surcharge, in order to complete your purchase.

In England and Northern Ireland the stamp duty surcharge is currently 5%. It is currently 8% in Scotland and there are different rates applicable in Wales. You will need the money to pay the stamp duty available at the time you complete your purchase.

For example, if you are purchasing a property for £500,000 in England before you have sold your current property, the stamp duty land tax (STLT), to be paid is £15,000 plus £25,000 (5% surcharge) = £40,000.

See our stamp duty calculator to work out exactly how much stamp duty you would need to pay.

The good news is, whilst you will have to pay the stamp duty surcharge to complete your purchase, you can claim this element back from HMRC, provided you sell your current property within 3 years.

If required, you can add the cost of the extra stamp duty to your loan, so that you don’t have to find the money for this upfront.

Last updated: 14 March 2026 | © KIS Bridging Loans 2024 | Privacy Notice | Complaints Policy