While many bridging loan lenders say they cover all of the UK, in practice borrowing is difficult in some places. The majority of lenders prefer to cater to urban areas, with a much smaller number operating in rural locations. Additionally, only a handful of lenders operate in Northern Ireland.

Historically, borrowers have found it difficult to take out bridging loans in Scotland but the number of lenders lending in Scotland has increased in recent years.

“At KIS Finance, we work with lenders right across the UK, many of whom don’t have a web presence. We can help you understand all of your options and secure a loan with the best possible rates based on your location.” Dan Wilkin, CEO KIS Finance

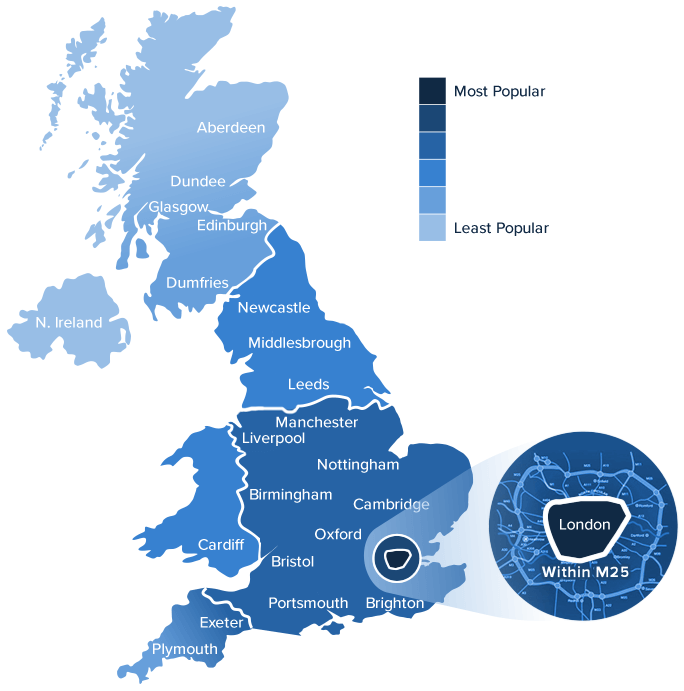

The map below illustrates where the majority of bridging lenders in the UK operate. As you can see, they tend to be clustered around the main cities like London, Edinburgh, Glasgow, Birmingham, Cardiff, and so on. London, in particular, has a very active residential and commercial property market, which has led to a high availability of bridging loans.

Most bridging loans are secured against property, the value of which is determined, in significant part, by its location. That’s the main reason why location affects availability.

Some of the factors tied up with location include:

Keep in mind that many lenders do not want to force the sale of properties secured against loans. It’s time-consuming and costly. They will also usually have to sell the property at a discount. As such, they can minimise risk by avoiding certain locations.

Most lenders operate in England and Wales, with a significant majority in and around urban centres. Large towns and cities tend to have active and steady housing markets with high liquidity (time to sale) and lots of demand.

Certain high-value property markets, such as the more expensive areas of London (Kensington, Chelsea, Knightsbridge, etc.), can present their own difficulties. Property is expensive in these areas and the market can sometimes be volatile.

More lenders have started to operate in Scotland in recent years. Historically, they had been reluctant to do so because of complex property sale and repossession laws. For example, the Debtors (Scotland) Act 1987 gives a certain degree of protection to debtors which can affect bridging loan lenders.

That said, Scotland has many good options, particularly in and around cities like Glasgow, Edinburgh and Aberdeen, all of which have active property markets.

Lenders tend to avoid Northern Ireland and it’s difficult, but not impossible, to secure bridging loans there.

Northern Ireland has a unique regulatory framework with many debtor-friendly protections and comparatively larger administrative burdens. This often results in higher rates and the need for an ironclad exit strategy (the means by which the loan will be repaid).

If you’re seeking a bridging loan in Northern Ireland, you’re likely to have more success if you work with an experienced broker like KIS Finance.

Location may have an influence on your access to bridging loans. The maximum possible size of finance facilities and interest rates also varies from region to region.

However, bridging loan lenders evaluate applications based on a range of factors, of which location is only one. Your exit strategy, which refers to how you’ll repay your loan and any associated interest, is what lenders are most interested in. The loan-to-value (LTV) ratio, the size of your loan compared to the security, is also very important.

Working with an experienced broker will ensure that you have access to all lenders in an area. Keep in mind that many lenders do not have an active online presence and work exclusively through brokers.

Written By Holly AndrewsLast updated: 20 February 2025 | © KIS Bridging Loans 2024 | Privacy Notice | Complaints Policy