Presented by KIS Finance

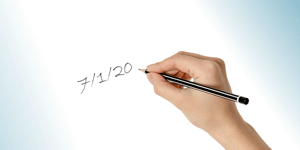

Most important legal documents and contracts that require a signature also require a date. It’s common practice to shorten the year when writing down a date, for example, last year you may have dated something as 7/1/19 – abbreviating 2019 to just 19.

Doing the same abbreviation this year, however, could cause all sorts of legal issues with paperwork and leave you at risk to fraud.

All dates can be altered, but this is a specific problem with the year 2020 as, if it is abbreviated to just 20, it will be very easy to alter. Simply adding two numbers to the end could easily change it to any year within this century. For example, 7/1/20 could be back-dated to 7/1/2019, or pushed forward to 7/1/2021. Being able to easily alter the date by just a year or two either way could make fraudulent documents difficult to detect.

If you have abbreviated 2019 to 19, however, the date could only be changed to a date before 2000, which is potentially very unrealistic depending on the type of document. This would be much easier to spot and dispute.

It’s very important when entering into any new financial contracts this year that you write the date out in full when you’re signing documents. This is especially important if you take out a short-term loan or bridging finance, where running over term can be very expensive.

For example, it may say in the contract that the loan needs to be repaid 12 months from the date it was taken out. If this was on 1st January 2020 and you signed the contract and wrote 1/1/20, the date could be changed by the lender or another party to 1/1/2019, simply by adding 19 to the end of the date. This could lead them to demand repayment straight away. With products like bridging loans there could also be large financial penalties for going over term, so this is something that could also be taken advantage of by anyone trying to defraud you for money.

Another way you could be caught out is if they backdate the contract, making it look like you’ve had the loan for a longer period of time, so they can charge you more in interest.

This is less likely to happen if you are dealing with reputable companies and lenders, so another reason to be cautious who you borrow money from. For more information please see our Fraud Guides section.

You also need to be thorough if you enter into any personal agreements or contracts this year. An example of this could be a contract between yourself and a friend if you loaned them some money. A contract of this sort would outline the terms of the agreement, including the date by which the money should be repaid by. If the date was abbreviated, then it could potentially be changed by the other party in order to add an extra year or two on to the repayment term.

When you start working for a new company, you should be given an employment contract to sign and date. This will outline the terms of your employment and confirm the date you started working for the company.

If you abbreviated 2020 to just 20 when you signed the contract, this could cause problems when it comes to your entitlement to certain statutory and contractual benefits, if the date were to be amended to a year or two later. This is because a lot of benefits, e.g. annual leave, contractual sick pay and contractual maternity pay, are determined by your length of service and your employer could get away with paying you less than what you’re entitled to.

If you buy or sell a vehicle within 2020, it’s very important to write the full date on any ownership documents. This is because future problems could occur if the vehicle was involved in any motoring offences, such as speeding, parking fines, or even criminal activity, with the new owner.

If the new owner received a large fine, they could change the date on the documents to make it appear as if you were the owner of the vehicle at the time of offence, making you potentially liable. This would obviously be open to dispute if you had evidence of the actual date where ownership was exchanged, but it would cause unnecessary problems that could have been avoided.

If you start a new tenancy this year, again, you must write the date in full when you sign and date your tenancy agreement. Problems could occur if the landlord were to change the date on the agreement to make it appear as if you lived in the property before you actually moved in, or you lived in the property after you had actually moved out. This would likely be in an attempt to make you liable for damages to the property that occurred before or after you were living there.

It’s important to make sure that all documents to do with any insurance policies show the right dates, in terms of cover start and expiry dates, and can’t be altered by somebody else as this could lead to problems should you need to make any claims.

So, this year before signing anything important, make sure to take care when writing out the date, either by writing it as 07/01/2020 or 7th January 2020, so it’s much harder to alter and you’re not leaving yourself open to potential fraud.

Find it useful? Please share!

Find it useful? Please share!

Last updated: 11 January 2022 | © KIS Bridging Loans 2024 | Terms & Conditions