Presented by KIS Finance

In this report we will be taking a look at the reasons why so many prospective homeowners are needing to rely on gifts, loans and inheritance from family to boost their finances in order to get on the property ladder.

According to the ONS (Office for National Statistics), in 2017, over half of first-time buyers were aged 34 or above.

This is a significant increase from before the last recession in 2007, when the average age was 28.[1] However, our data shows that some people are having to wait far beyond this age before having the funds available to put down a house deposit.

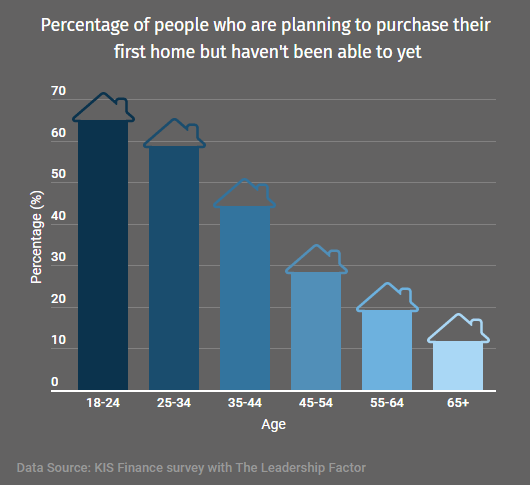

A staggering 44.2% of the 35-44 year-olds who took part in our survey are planning to purchase their first home but haven’t been able to yet. 17% of this age group have stated that they will still need help from family to put the deposit together.

More significantly, 28.3% of 45-54 year-olds are still waiting to purchase their first home and 7.6% of this group will be relying on financial help from family to make this happen.

So why is it taking people so much longer to get on the property ladder and how is this having an impact on people’s finances?

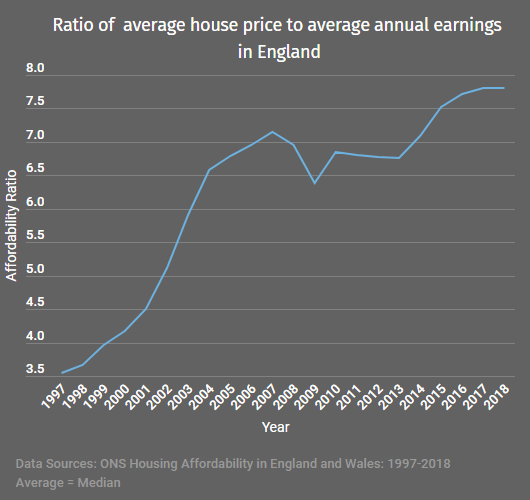

Taking a look at the latest house price to earnings ratio, on average, we can now be expected to have to spend 7.8 times our annual income to purchase a home in England. This figure has been on a steadily upward trend over the last 20 years, rising from just 3.5 in 1997.[2]

Looking across the country, there are huge regional differences. Buying a house in the North West of England will cost, on average, 2.5 times the average national annual salary, whilst in London this figure rises to as much as 44.5 times for those buying in areas like Kensington and Chelsea.[2]

With housing becoming continuously less affordable over such a long period of time, this is having a big impact on peoples' ability to buy their first home.

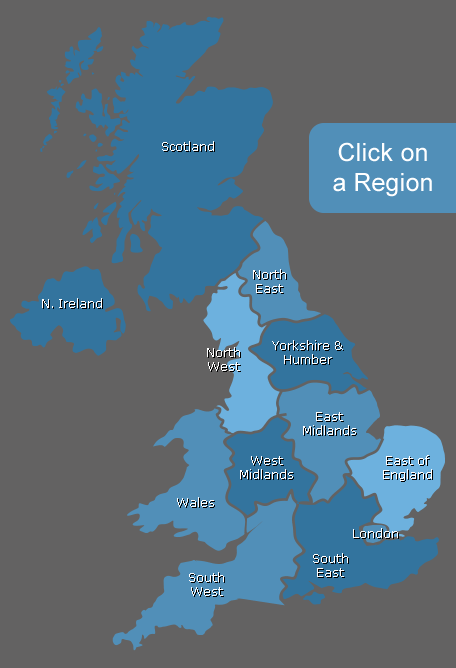

In the interactive map below, you can see how long it would take to save an average deposit in each region of the UK based on average house prices.[5] [6] [7] We’ve looked at the time it will take, based on the average UK salary per age group[4], depending on whether you save 10% or 20% of your monthly income.

| Average House Price: | £150,825 |

| Average Deposit (20%): | £30,165 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 8 Years, 8 Months |

| 22-29 | 6 Years, 1 Month |

| 30-39 | 4 Years, 10 Months |

| 40-49 | 4 Years, 6 Months |

| 50-59 | 4 Years, 11 Months |

| 60+ | 5 Years, 8 Months |

| Age | Time |

| 18-21 | 17 Years, 4 Months |

| 22-29 | 12 Years, 2 Months |

| 30-39 | 9 Years, 8 Month |

| 40-49 | 9 Years, 1 Month |

| 50-59 | 9 Years, 10 Months |

| 60+ | 11 Years, 4 Months |

| Those reliant on family to fund deposit on first home | 14.1% |

| Those reliant on family to cover living expenses | 14.8% |

| Those planning to never buy their own home | 10.1% |

| Average House Price: | £134,811 |

| Average Deposit (20%): | £26,962 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 7 Years, 9 Months |

| 22-29 | 5 Years, 5 Months |

| 30-39 | 4 Years, 4 Months |

| 40-49 | 4 Years |

| 50-59 | 4 Years, 5 Months |

| 60+ | 5 Years, 1 Month |

| Age | Time |

| 18-21 | 15 Years, 6 Months |

| 22-29 | 10 Years, 10 Months |

| 30-39 | 8 Years, 7 Months |

| 40-49 | 8 Years, 1 Month |

| 50-59 | 8 Years, 10 Months |

| 60+ | 10 Years, 1 Month |

| Those reliant on family to fund deposit on first home | 8.2% |

| Those reliant on family to cover living expenses | 22.4% |

| Those planning to never buy their own home | 8.2% |

| Average House Price: | £471,504 |

| Average Deposit (20%): | £94,300 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 27 Years, 1 Month |

| 22-29 | 19 Years |

| 30-39 | 15 Years, 1 Month |

| 40-49 | 14 Years, 2 Months |

| 50-59 | 15 Years, 4 Months |

| 60+ | 17 Years, 8 Months |

| Age | Time |

| 18-21 | 54 Years, 2 Months |

| 22-29 | 38 Years |

| 30-39 | 30 Years, 1 Month |

| 40-49 | 28 Years, 4 Months |

| 50-59 | 30 Years, 8 Months |

| 60+ | 35 Years, 4 Months |

| Those reliant on family to fund deposit on first home | 30.7% |

| Those reliant on family to cover living expenses | 28.3% |

| Those planning to never buy their own home | 6.8% |

| Average House Price: | £161,891 |

| Average Deposit (20%): | £32,378 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 9 Years, 4 Months |

| 22-29 | 6 Years, 6 Months |

| 30-39 | 5 Years, 2 Months |

| 40-49 | 4 Years, 11 Months |

| 50-59 | 5 Years, 3 Months |

| 60+ | 6 Years, 1 Month |

| Age | Time |

| 18-21 | 18 Years, 7 Months |

| 22-29 | 13 Years |

| 30-39 | 10 Years, 4 Months |

| 40-49 | 9 Years, 10 Months |

| 50-59 | 10 Years, 6 Months |

| 60+ | 12 Years, 2 Months |

| Those reliant on family to fund deposit on first home | 19.2% |

| Those reliant on family to cover living expenses | 23.5% |

| Those planning to never buy their own home | 11.5% |

| Average House Price: | £130,888 |

| Average Deposit (20%): | £26,177 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 7 Years, 6 Months |

| 22-29 | 5 Years, 3 Months |

| 30-39 | 4 Years, 2 Months |

| 40-49 | 3 Years, 11 Months |

| 50-59 | 4 Years, 3 Months |

| 60+ | 4 Years, 11 Months |

| Age | Time |

| 18-21 | 15 Years |

| 22-29 | 10 Years, 6 Months |

| 30-39 | 8 Years, 4 Months |

| 40-49 | 7 Years, 10 Months |

| 50-59 | 8 Years, 6 Months |

| 60+ | 9 Years, 10 Months |

| Those reliant on family to fund deposit on first home | 20.8% |

| Those reliant on family to cover living expenses | 22.6% |

| Those planning to never buy their own home | 6.6% |

| Average House Price: | £161,443 |

| Average Deposit (20%): | £32,288 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 9 Years, 3 Months |

| 22-29 | 6 Years, 6 Months |

| 30-39 | 5 Years, 2 Months |

| 40-49 | 4 Years, 10 Months |

| 50-59 | 5 Years, 3 Months |

| 60+ | 6 Years, 1 Month |

| Age | Time |

| 18-21 | 18 Years, 7 Months |

| 22-29 | 13 Years |

| 30-39 | 10 Years, 4 Months |

| 40-49 | 9 Years, 8 Months |

| 50-59 | 10 Years, 6 Months |

| 60+ | 12 Years, 1 Month |

| Those reliant on family to fund deposit on first home | 24% |

| Those reliant on family to cover living expenses | 25.5% |

| Those planning to never buy their own home | 6.4% |

| Average House Price: | £192,682 |

| Average Deposit (20%): | £38,536 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 11 Years, 1 Month |

| 22-29 | 7 Years, 10 Months |

| 30-39 | 6 Years, 2 Month |

| 40-49 | 5 Years, 10 Months |

| 50-59 | 6 Years, 3 Months |

| 60+ | 7 Years, 3 Months |

| Age | Time |

| 18-21 | 22 Years, 2 Month |

| 22-29 | 15 Years, 6 Months |

| 30-39 | 12 Years, 4 Months |

| 40-49 | 11 Years, 6 Months |

| 50-59 | 12 Years, 6 Months |

| 60+ | 14 Years, 6 Months |

| Those reliant on family to fund deposit on first home | 20.5% |

| Those reliant on family to cover living expenses | 15.9% |

| Those planning to never buy their own home | 7.9% |

| Average House Price: | £289,436 |

| Average Deposit (20%): | £57,887 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 16 Years, 8 Months |

| 22-29 | 11 Years, 8 Months |

| 30-39 | 9 Years, 3 Months |

| 40-49 | 8 Years, 8 Months |

| 50-59 | 9 Years, 5 Months |

| 60+ | 10 Years, 11 Months |

| Age | Time |

| 18-21 | 33 Years, 4 Months |

| 22-29 | 23 Years, 4 Months |

| 30-39 | 18 Years, 6 Months |

| 40-49 | 17 Years, 4 Months |

| 50-59 | 18 Years, 10 Months |

| 60+ | 21 Years, 10 Months |

| Those reliant on family to fund deposit on first home | 20.3% |

| Those reliant on family to cover living expenses | 21.5% |

| Those planning to never buy their own home | 8.9% |

| Average House Price: | £318,727 |

| Average Deposit (20%): | £63,745 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 18 Years, 4 Months |

| 22-29 | 12 Years, 10 Months |

| 30-39 | 10 Years, 2 Months |

| 40-49 | 9 Years, 7 Months |

| 50-59 | 10 Years, 5 Months |

| 60+ | 12 Years |

| Age | Time |

| 18-21 | 36 Years, 7 Months |

| 22-29 | 25 Years, 8 Months |

| 30-39 | 20 Years, 4 Months |

| 40-49 | 19 Years, 2 Months |

| 50-59 | 20 Years, 10 Months |

| 60+ | 23 Years, 11 Months |

| Those reliant on family to fund deposit on first home | 22.3% |

| Those reliant on family to cover living expenses | 19.1% |

| Those planning to never buy their own home | 9.6% |

| Average House Price: | £253,410 |

| Average Deposit (20%): | £50,682 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 14 Years, 7 Months |

| 22-29 | 10 Years, 2 Months |

| 30-39 | 8 Years, 1 Month |

| 40-49 | 7 Years, 7 Months |

| 50-59 | 8 Years, 2 Months |

| 60+ | 9 Years, 6 Months |

| Age | Time |

| 18-21 | 29 Years, 1 Months |

| 22-29 | 20 Years, 4 Months |

| 30-39 | 16 Years, 2 Months |

| 40-49 | 15 Years, 2 Months |

| 50-59 | 16 Years, 5 Months |

| 60+ | 19 Years |

| Those reliant on family to fund deposit on first home | 37.9% |

| Those reliant on family to cover living expenses | 24.2% |

| Those planning to never buy their own home | 6.1% |

| Average House Price: | £195,498 |

| Average Deposit (20%): | £39,099 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 11 Years, 2 Months |

| 22-29 | 7 Years, 10 Months |

| 30-39 | 6 Years, 3 Months |

| 40-49 | 5 Years, 11 Months |

| 50-59 | 6 Years, 4 Months |

| 60+ | 7 Years, 4 Months |

| Age | Time |

| 18-21 | 22 Years, 5 Months |

| 22-29 | 15 Years, 8 Months |

| 30-39 | 12 Years, 6 Months |

| 40-49 | 11 Years, 10 Months |

| 50-59 | 12 Years, 8 Months |

| 60+ | 14 Years, 8 Months |

| Those reliant on family to fund deposit on first home | 20.9% |

| Those reliant on family to cover living expenses | 14.1% |

| Those planning to never buy their own home | 5.6% |

| Average House Price: | £163,902 |

| Average Deposit (20%): | £32,780 |

| 20% of Income | 10% of Income |

| Age | Time |

| 18-21 | 9 Years, 5 Months |

| 22-29 | 6 Years, 7 Months |

| 30-39 | 5 Years, 3 Months |

| 40-49 | 4 Years, 11 Months |

| 50-59 | 5 Years, 4 Months |

| 60+ | 6 Years, 2 Months |

| Age | Time |

| 18-21 | 18 Years, 10 Months |

| 22-29 | 13 Years, 2 Months |

| 30-39 | 10 Years, 6 Months |

| 40-49 | 9 Years, 10 Months |

| 50-59 | 10 Years, 8 Months |

| 60+ | 12 Years, 4 Months |

| Those reliant on family to fund deposit on first home | 23.8% |

| Those reliant on family to cover living expenses | 19.8% |

| Those planning to never buy their own home | 11.1% |

* This data is based on ONS' UK median full-time gross weekly earnings (April 2018)[4], broken down by age group. The data shows the length of time it would take an individual to save for an average house deposit if the individual were to stay on that income for the full duration and saved either 20% or 10% of their earnings per month.

** This data is from KIS Finance’s survey with The Leadership Factor.

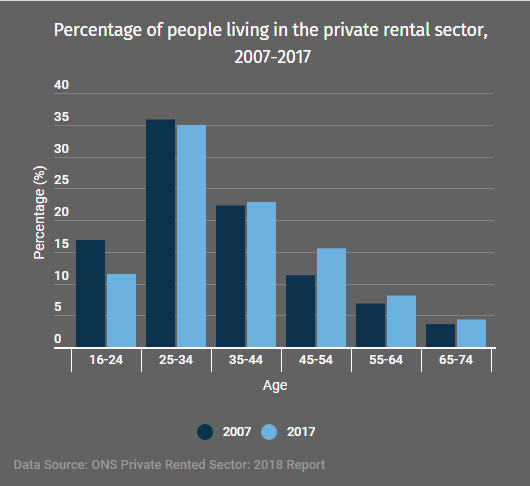

In 2007 there were 2.8 million households in the private rental sector. This number has grown by an average of 200,000 properties per year to reach a whopping 4.5 million in 2017.[8]

The graph below shows the percentage of people living in private rental properties, split by age group. What’s surprising to see is that rental households are actually getting older, with the biggest increase being the number of 45-54 year-olds living in rented property.

Unsurprisingly, 16-24 year-olds are still the largest group living in the private rental sector, although, this group has seen the biggest decrease in numbers over the past decade as more young adults are opting to live at home with their parents for longer. The number of young adults living at home between the ages of 18 and 34 has increased, with the largest jump being the number of 24 year olds, which has risen by 12% since 1997.[1]

With the overall number of people living in rented accommodation increasing and rental prices having gone up by a whopping 7.7% in the four years since 2015[9], it’s clear that this may be a contributing factor as to why so many people are needing help from family to get on the property ladder.

In the wake of the last recession, mortgage lenders have significantly tightened their lending criteria, making it all the more difficult for first time buyers to get a mortgage, even if they have been able to scrape the deposit together.

With concerns about avoiding bad debts, new rules have been introduced which require borrowers to prove that they can still afford their mortgage, even if the interest rate was to rise by 3% above the variable rate at the end of their introductory offer. This level of ‘stress testing’ means that some first time buyers are struggling to prove that they can afford the size of mortgage that they need to buy their own home.

The amount that they can borrow has also been hit by a tightening up on the loan to value criteria that lenders will allow. In 2007, 14.1% of new mortgages were for loans of over 90%, with 5.6% being for over 95% of the property’s value. But by 2019 this figure has reduced to only 4.5% for loans over 90% and a tiny 0.2% of mortgages were for over 95% of the property’s value. This means that borrowers are having to find larger deposits than ever before to make up for this shortfall in lending.[10]

With total gross mortgage advances in the UK falling by 34% from 2007 to 2018 it’s not surprising that many are struggling to get the finance that they need.[10]

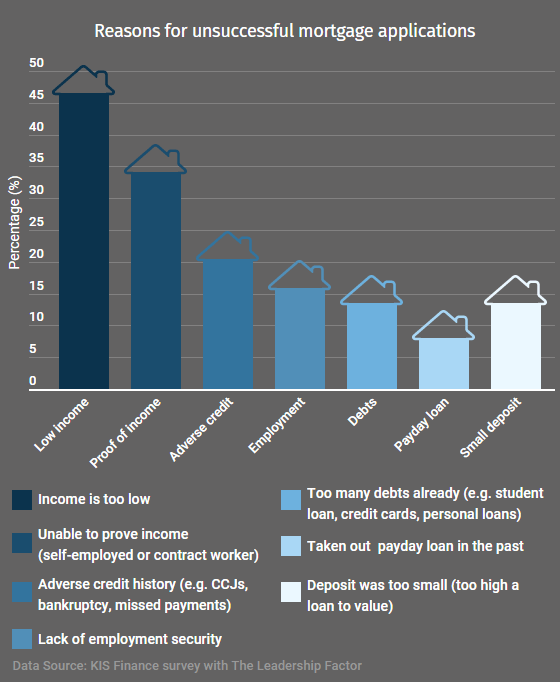

Our survey asked those who have applied for a mortgage, but were declined, the reasons they were given as to why their application wasn't accepted. The results are displayed in the graph below.

As you can see, the majority of declined applications are caused by issues surrounding income - the largest percentage being applicants having too low an income altogether, and the second being those with an inability to prove sufficient income due to being self-employed or a contract worker.

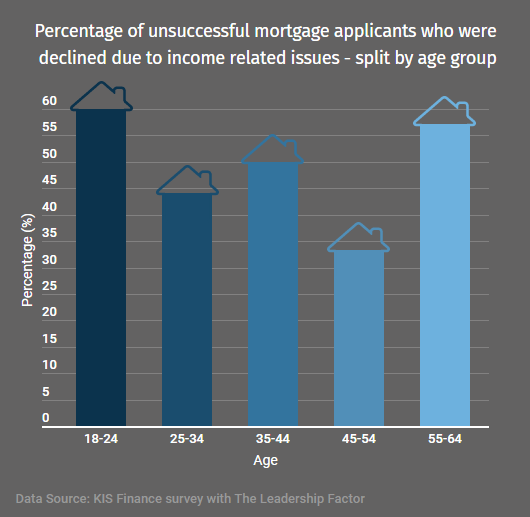

When we broke this data down by age group, unsurprisingly 18-24 years-olds represented the largest group who have been declined a mortgage based on low income, with 62.5% having been turned down. However, the second largest group in this category is 55-64 year-olds where 57.1% of those who were declined a mortgage reported that this was due to income related issues.

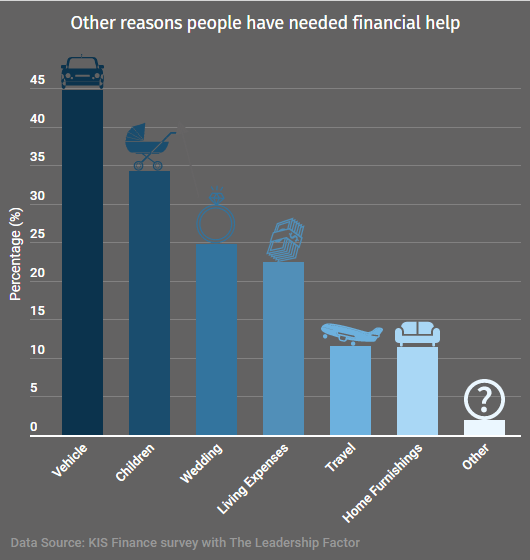

It’s not just first homes that Brits are needing help to purchase – a massive 44.8% of our respondents said they have received help from family members to purchase a car and to cover its running costs (maintenance, insurance etc).

The second most common reason for a family loan was to cover the costs of having children – initial costs of having a baby (buying prams, cots, clothes etc), childcare and school fees etc.- with 34.4% of respondents having said they have received financial help for these reasons.

More worryingly, 22.4% of respondents said that they have had to receive help from family to cover general day to day living expenses, including rent, bills and shortfalls in wages.

This data shows that it's not just big purchases and financial commitments that people are struggling to make, but actually some are needing help just to make ends meet.

With it not looking like it will become any easier for people to get that first foot on the property ladder anytime soon, it looks like people will have to continue relying on help from family and friends to buy their first home.

Sources of data

All figures, unless otherwise stated are from The Leadership Factor – total sample size was 2,002. Fieldwork was undertaken between 17th June 2019 and 24th June 2019. The survey was carried out online. View The Leadership Factor report here.

Other data sources

Find it useful? Please share!

Last updated: 23 January 2020 | © KIS Bridging Loans 2024 | Terms & Conditions