Presented by KIS Finance

In London the problem is at its greatest with over 1 in 5 people reporting that they have delayed making key financial decisions as a direct result of Brexit. With around 15% in Wales (that’s 1 in 6) and 14% in Scotland, similarly affected, the problem is clearly a national one.

Those aged between 25 to 49 report being the most affected by delaying major spending, with 16% claiming their decisions are delayed due to Brexit. With the average age of a first time home buyer in the UK being 30 (6 years older than the average in 1980), delays for this age group could make getting on the property ladder even harder. It’s already tricky enough for young people to buy their first home without having to face additional hurdles.

People are clearly tired of the continuing uncertainty and want an end to the whole Brexit mess. We asked Brits through our survey how they would vote if given the choice now of remaining in the EU or leaving on the terms set out in Theresa May’s deal. Of the people who confirmed they would vote, and currently have a preference, 61% stated they wanted the UK to remain in the EU.

However, when given a third option of leaving without a deal, the results were as follows:

Nearly 3 times as many people confirmed they would vote for a ‘no deal’ exit rather than accept the terms negotiated by the Government.

Clearly people are looking for an end to the matter but would prefer taking the drastic step of leaving the EU without a negotiated deal rather than accept the compromise of the current deal on the table.

According to the Office for Budget Responsibility, activity in the housing market is predicted to remain fairly subdued in the short-to-medium term. Current predictions for 2019 stand at 1.17m property sales, which is around 2% less that the total sales of 1.19m recorded in 2018. At a time when wage growth and employment levels are strong, we would expect to see a strong increase in house sales. However, Brexit uncertainty seems likely to be the key factor affecting the housing market, as people delay buying and selling in the current climate.

London has been hardest hit with house prices slowly declining since 2017 and with no current end in sight to the Brexit debacle, the slide looks likely to continue. In fact, a recent report from the Royal Institution of Chartered Surveyors described the outlook for house sales in London as the most negative for the last 20 years.

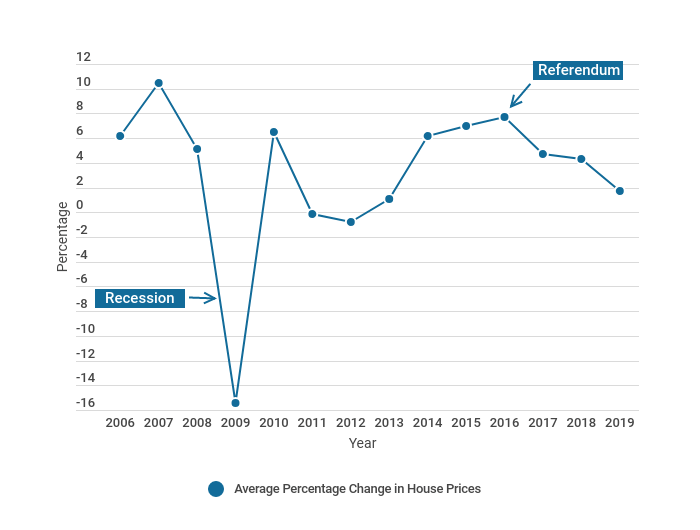

The average increase in house prices, which stood at 1.7% at the beginning of the year, shows a significant drop since 2016 when increases of 7.7% were seen. As the graph below shows, this worrying decline in the growth of house prices shows similar patterns to those seen in the last recession, which are likely to continue until consumer confidence returns and house sales pick up.

Since the referendum, growth levels for new housing have dropped significantly. Growth in residential construction is struggling to keep pace with the level of need, fuelling the current housing crisis.

Increasing caution by developers not to over commit themselves during the current turbulent times has led to net housing additions that are around 26% below the government’s annual target of 300,000 new houses a year, that’s 78,000 homes. According to Knight Frank’s most recent housebuilders survey, only 1% of developers who responded thought that a growth rate of more than 300,000 new homes per year was actually achievable by 2022. In fact, forecasts from the Construction Industry Training Board (CITB) and Experian predict that growth in the private housing sector could fall to 0% by 2021. Therefore, the sooner there is clarity over Brexit, the sooner the construction sector will be able to commit to investment for the future.

Since the referendum the demand for bridging finance has remained high, but an increasing percentage of customers are now focused on re-financing and re-bridging, as people are affected by tightening markets. Rather than helping them to move forward, bridging is frequently being used as a way to weather the current storm.

Those who already have bridging finance may find they need to re-bridge as they have been unable to sell a property that they were relying on as their exit strategy. This is particularly the case with higher value properties, especially in London, where the market has slowed linked to the current uncertainty. For example, a property with an estimated value of £6million was recently valued at £2.75million under a 90 day valuation, as surveyors express concern at the ability to shift property at the top end of the market in the current climate.

Of course those who want to buy now to take advantage of lower prices are frequently opting to take out a bridging loan to enable them to complete their purchase before securing a buyer for their own property.

Some lenders are responding to the current climate by reducing the ‘Loan to Value’ that they will lend on, which has been further depressing the market as a whole by making it harder for borrowers to qualify for property-backed loans. This tightening of the market is worryingly very reminiscent of the last credit crunch.

Some funding lines have also been adversely affected, especially those from the USA, who see Europe as a safer option than the UK at present.

Andrew Calf, operations manager at London based PB Supercar Hire, had plans in progress to move to larger business premises in March 2018 after a deal for £4.2 million was agreed with the vendor.

“A legal delay pushed the move back to December 2018, so I was forced to pull out of the deal due to the falling property market caused by Brexit uncertainty towards the end of the year. The commercial premises also came with 8 residential flats which could lose us a fortune if no deal goes ahead. Being forced to lose this commercial property means that our expansion plans are now on hold as the vendor refuses to reduce his price or split the freehold. I was planning on taking on 3 more members of staff which now can’t happen."

Michael Patterson, CEO of We Buy Any House has provided the following comment on customers’ biggest concerns when it comes to Brexit:

‘We speak to hundreds of customers each day, many of whom are looking to sell their property quickly so that they can relocate before the Brexit storm hits. A lot of the conversations we have with customers are around what Brexit could mean for the property industry and what it may mean for selling their property. Traditional house sale routes have begun to stagnate as many buyers baton down the hatches to hold out until there’s more clarity around Brexit and its potential effects. The reality of the matter is that, because there are no parallels, predicting what it could mean for house sales for our customers is proving difficult. What we do know is that in times of political and economic uncertainty, the property market is often the hardest hit.’

Holly Andrews, Managing Director at KIS Finance commented on the situation:

“We’ve seen a definite increase in the demand for re-bridging finance as properties are not selling as quickly. We are also doing more re-mortgages now than we were before due to people choosing to stay put and sit out Brexit uncertainty. To date, we’ve not seen any rate changes related to Brexit on the mortgage front, but with bridging, the Loan to Value limits are dropping with some lenders and underwriters being more cautious with their lending decisions. The longer the whole Brexit debate continues, and people delay making key financial decisions, the more significant the problems for the finance sector will become”.

Sources of data

All figures, unless otherwise stated, are from YouGov Plc. Total sample size was 1,787 adults. Fieldwork was undertaken between 23rd - 24th April 2019. The survey was carried out online. The figures have been weighted and are representative of all GB adults (aged 18+). View YouGov Report

Other data sources

www.landregistery.data.gov.uk

www.citb.co.uk

Find it useful? Please share!

Last updated: 23 January 2020 | © KIS Bridging Loans 2024 | Terms & Conditions