Presented by KIS Finance

Ironically APRs were introduced in an effort to improve the fairness and transparency of the lending market. Before APRs were a legal requirement finance adverts could be very misleading. For example, car finance could be advertised simply as 8%, but customers wouldn’t have known if this was an annual rate, flat rate or even a monthly rate of interest. Therefore companies could advertise what appeared to be an attractive rate but turned out to be far from a good deal.

In some cases finance could even be advertised as 0% but without making it clear that there were hefty set up fees involved. For example a £5,000 hire purchase agreement could actually wind up costing £10,000 over a 3 year term, despite the 0% interest rate, due to £5,000 of fees.

APRs were introduced to provide a level playing field so that customers could compare the full cost of finance. Whatever the interest rate being charged was, the method by which it was charged, and any costs associated with setting up, or arranging the finance, these would be taken into account within the advertised APR. This meant that customers could easily compare different loan companies, credit card and car finance providers, to find the best deal.

It wasn’t long until some lenders found a way to manipulate APRs, and this was by introducing payment protection insurance, also known as Sickness, Accident and Redundancy cover, PPI or SAR.

Insurance cover was not included in the APR calculation, which led to lenders placing insurance cover on their finance facilities, which they would then load the price of. This enabled them to reduce their interest rate or fees, meaning they could advertise a lower APR, giving them an advantage over their competitors. Although they weren’t making so much profit on the interest charges, the lenders were now able to make this up on the insurance cover.

In order to be able to compete, the majority of the lenders all followed suit, leading to the huge growth in the payment protection business throughout the 1990s and 2000s.

The FCA began imposing fines for mis-selling PPI in 2006 and the situation escalated in 2008 when Which? reported that 1 in 3 PPI customers had a “worthless” policy. Since then the number of claims have rocketed and by the claims deadline of 29 August 2019 it’s estimated that £36billion will have been paid out in compensation.

Whilst every cloud has a silver lining, the huge sums of compensation paid out over the last decade may have helped stimulate the economy into a quicker post-recession recovery. Acting in the same way as tax cuts, with average refunds of around £2000, this cash injection has noticeably boosted spending across the country.

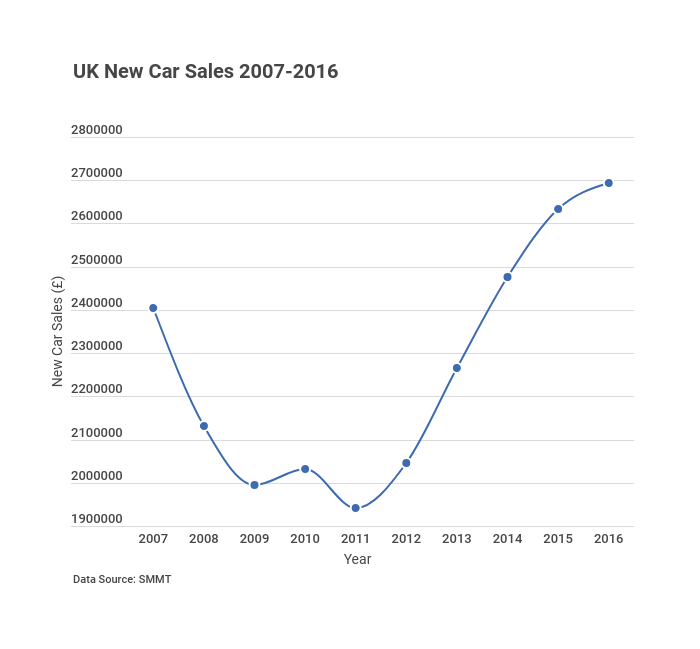

Households receiving a substantial but unexpected sum may have chosen to splash out on items such as home improvements, luxury items and cars. Certainly there was a steady decline in new car sales from 2003 to 2011, but from 2011 to 2016 the market saw a steady increase. This is interesting as the banks lost a Judicial Review in 2011, meaning that it became harder for them to defend PPI mis-selling complaints. As a result, a higher proportion of complaints were upheld, leading to more refunds, which in turn encouraged more customers to complain and generate further refunds.

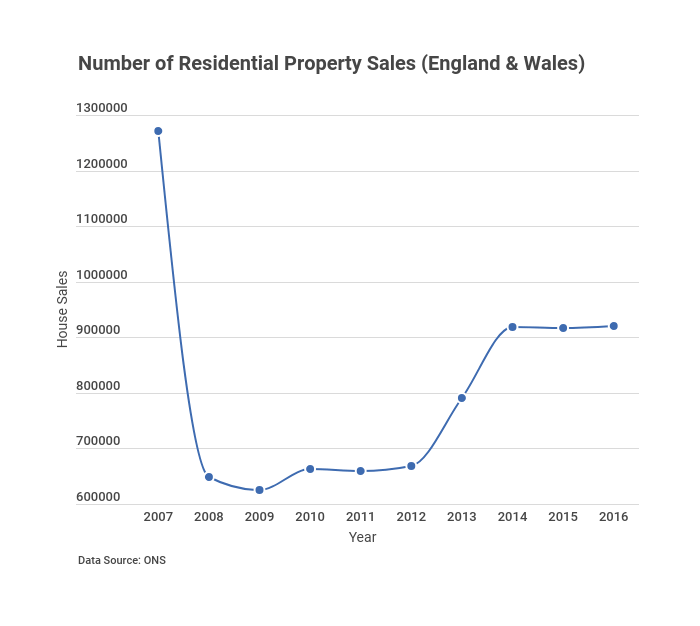

With some refunds being for much larger sums, this may have even been a factor in supporting the housing market during a time of recession. For some an unexpected lump sum may have helped contribute to a deposit and enabled them to get started on the housing ladder. The fact that having stagnated since 2008, the housing market started a period of steady growth in 2011, suggests that this could have been supported by PPI refunds.

With the deadline at the end of August signalling the end of the PPI refund bonanza, what’s next on the horizon? We’re already seeing an increase in the number of adverts targeting those who have lost out on investments or pensions, promising compensation following receipt of poor advice from banks and financial institutions.

Whilst this may seem like good news to those who have lost out, lenders have already tightened their criteria over recent years in an effort to reduce their exposure to risk. This means that many customers will continue to lose out if it becomes increasingly difficult to get credit or be accepted for a mortgage.

It’s easy to assume that PPI is a useless product based on the negative media coverage and how it was mis-sold. But sold correctly payment protection policies have their place, providing security that your payments will be covered should you become sick or made redundant.

However in the wake of the PPI scandal it’s now virtually impossible to find lenders willing to provide this type of cover. Banks have taken a complete U turn from implying that you must have PPI in order to be eligible for a loan or credit card, to not offering PPI at all. Customers are now borrowing money without any discussion as to how they will meet their monthly payments if they are suddenly unable to work.

We approached two of the large banks, Barclays and RBS, to see how easy it was to purchase cover from them. In both cases, staff tried to refer us to the PPI claims team despite our explaining that we were looking to take out cover on a loan and were not trying to make a complaint. Staff at both banks were initially unable to clarify if they still offered cover, before confirming that they actually no longer did.

You can still go on-line to obtain a quote for various types of cover from insurance companies, but it’s now up to the customer to identify gaps in their own provisions and arrange the right insurance. The risk is that many of us may now find ourselves in trouble if the unexpected happens and we can no longer afford to meet the payments on loans and credit agreements.

Find it useful? Please share!

Last updated: 23 January 2020 | © KIS Bridging Loans 2024 | Terms & Conditions