Presented by KIS Finance

With the news full of concerns over rising prices, many UK households are finding themselves increasingly worse off at the end of every month. Today’s announcement that the Bank of England has decided to hold interest rates at 0.1% is good news, but for numerous people their real standard of living continues to fall.

"With many of the current inflationary pressures due to global factors, simply raising interest rates may not ease the problem. It is more likely to have added to the misery that households are currently facing, which is probably a key factor in the Bank of England’s decision today to hold interest rates at their lowest ever level."

KIS Finance has been investigating whether the cost of living has risen disproportionally over time and why people are now struggling more than ever to make ends meet.

Whilst households in previous generations tended to consist of one main breadwinner, today most households rely on two incomes to get by. The real value of wages has overall be falling for many years, with the Office of Budget Responsibilities predicting that real UK wages will be lower in 2026 than they were in 2008.

As we come out of the pandemic, the estimated growth in average earnings for next year stands at 3.9%, but with Consumer Price Index (CPI) inflation predicated to reach 4.4% the real value of the money in our pockets will continue to fall. In fact, the 1.2% jump in inflation rates between July and August this year was the largest rise since records began in 1997 and, more bad news, rates are predicted to continue to rise for some time.

Inflation measures the increase in the price of goods and services over time, usually on a monthly or annual basis.

So if your disposable income is £1,000 per month and you spend all of this, then a 3.9% increase in earnings will give you a new monthly disposable income of £1,039. However, if inflation is running at 4.4% your outgoings will increase to £1,044 per month, meaning that you will need to cut your expenditure by £5 and reduce what you buy to balance this out.

The Office of National Statistics tracks inflation by looking at the value of a set “basket of goods” to monitor how prices are rising. This measure is known as the Consumer Price Index and the contents of the “basket” are regularly reviewed to reflect changing consumer habits.

Interestingly, during the pandemic sandwiches bought in staff restaurants were removed as one of the measures, but the price of hand sanitisers and men’s loungewear bottoms were added to reflect changing demand and expenditure patterns.

It seems that costs in every area of life are currently increasing. Energy prices are soaring, affecting both individuals and businesses. Whilst households are seeing their energy bills rapidly increase, industries that rely on power for machinery, equipment, heating and lighting offices, are having to absorb the additional costs, putting pressure on prices for a range of items.

Industry experts are predicting that natural gas prices won’t fall until well into 2022 and given that natural gas is a crucial element in the production, storage, and transport of a wide range of everyday products, this will push prices up further.

The government is also winding back the additional support that they provided to some sectors during the pandemic, such as tax breaks for pubs and restaurants. Whilst the autumn budget saw a reduction in tax on sparkling wine and draught beer, stronger drinks such as red wine and spirits saw a tax increase. So once again customers are likely to be left facing higher prices and dining out will become an unaffordable luxury for many.

Food prices are also increasing at an unprecedented rate. Supermarket prices increased by 1.1% in August, which was the sharpest rise since the financial crash in 2008. Part of the problem is down to supply chain issues, which are pushing prices up. However, there are longer terms problems in the shape of limited farmland for growing food and the rapidly increasing world population, which according to the Chief Executive of Kraft Heinz, Miguel Patricio, means that higher food prices are here to stay.

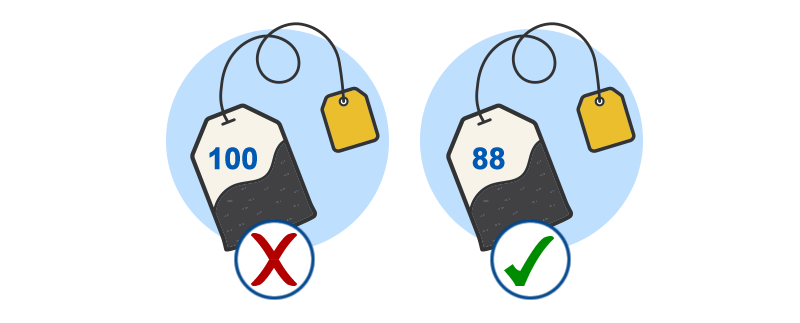

Some price increases have been subtly hidden by manufacturers, who have controlled their costs by reducing product sizes, whilst maintaining the original price. Often referred to as ‘shrinkflation’, manufacturers have been using this approach for some time, with some memorable examples, such as the increase in the size of the gaps on a Toblerone bar, which previously made the headlines. The public outcry was so great that the manufacturers, Mondelez International, eventually reverted back to the original shape but put the price up! Birds Eye reducing the number of fishfingers in a packet from 12 to 10 and Tetley Teabags now coming in packets of 88 rather than 100, are proof that this approach is becoming more common, with customers losing out as their money no longer buys the same amount as it once did.

Competition for staff in some sectors has pushed wages up, as companies vie with each other to attract and retain employees. Hospitality, retail, and transport are all reporting staff shortages and are left to desperately try to attract staff into the sector.

This has added another upwards pressure on prices, as employers have to meet these additional costs and are often left with no alternative than to pass this on to customers via price increases.

Whilst some may be lucky enough to see pay rises in line with inflation, most won’t benefit from this and will see their income fall in real terms.

Some companies are dealing with rising labour costs by simply reducing staffing numbers, which means that whilst employees may benefit from a higher salary, they are having to work harder to absorb the reductions in staffing numbers. So their quality for life and work / life balance is also suffering as a result of the changes.

Some inflation is actually needed in a healthy economy, if prices are stagnant or falling then people may hold off spending to see if prices will fall even lower, which can have a negative effect on the economy as a whole. That’s why the Bank of England aims to keep inflation around 2% to ensure things tick along.

However, with current predictions expecting inflation to rise to over twice this level, the Bank of England may still decide to raise interest rates in the future as part of a strategy to try to control spending. This will of course add even more pressure to already stretched households, as many people could see monthly payments go up.

Whilst there will still be the demand for essential items, spending on non-essentials will fall, impacting sectors such as hospitality and travel. Having already been hard hit by the pandemic, this is a further blow to their recovery and could put more jobs at risk.

According to the think tank Demos, those aged 18 – 30 have been hardest hit by the current financial challenges caused by rising prices and falling real wages. They describe this age group as facing the “greatest uphill battle” to make ends meet. As the age band with, on average, the highest debt levels, and lowest incomes, many have little room to accommodate increasing costs and certainly the future looks likely to be a challenging one.

Holly Andrews, Managing Director at KIS Finance says:

“As the increases in the cost of living continues to outstretch wage rises for many, the impact is really being felt across the country. Those trying to get onto the property ladder for the first time are seeing their dreams disappear as they struggle to meet affordability criteria due to a fall in their real wages. Once general expenditure is taken into account their amount of disposable income has been badly eroded by the current increase in costs across the economy. With the cost of food and bills escalating many are now failing affordability tests when they come to apply for a mortgage. Even with the Bank of England’s decision not to increase interest rates at the present time, buying their own home may now become simply too expensive for many young people.”

Find it useful? Please share!

Last updated: 04 November 2021 | © KIS Bridging Loans 2024 | Terms & Conditions