Presented by KIS Finance

By 4th April 2018 all private or voluntary sector employers with 250 or more relevant employees must publish data on several key metrics, which are designed to show the size of the pay gap between all their male and female employees. The “snapshot date" for this data is the 5th April each year, meaning that data published this year will relate to April 2017.

The organisation will constitute as a ‘relevant employer’ if they have 250 or more employees that are based in England, Wales or Scotland. The legal entity muster register and report to the Gender Pay Gap Reporting Service.

If the organisation has multiple payrolls, for different departments, the relevant data from all payrolls must be merged together and reported as one set of figures.

The ‘relevant employees’ for the report include;

Self-employed: You must include self-employed workers in your figures if they personally provide work for you and you have the relevant data available to add to your figures.

Part-time employees: Any part-time employees in your organisation must also be included in the calculations.

Job shares: If you have any job-share arrangements in your organisation, each person in a job-share counts as one employee for the report.

Overseas workers: You must include any employees that are based overseas if they have a contract of employment that is subject to English, Welsh or Scottish law.

Partners: You don’t need to include any partners that you have within a partnership. This is because they take a share of the profits which isn’t comparable with the pay of an employee.

You do not have to include employees who are being paid at a reduced rate or not at all due to being on leave for one of the following reasons:

However, if you pay bonuses, these employees would need to be included in the calculation.

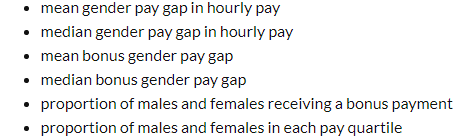

You must publish the following:

You must publish the information within 12 months of the snapshot date. As the snapshot date is 5 April it must therefore be published by 4 April the following year. It does not necessarily have to be published at the same time every year.

For the purposes of GPG reporting, "ordinary pay" is defined as:

However, the following are specifically excluded from ordinary pay:

For the purposes of GPG reporting, the basic unit of data that will be used in the calculations is the "hourly rate of pay". To work out the hourly rate of pay for each employee, you should follow the following five steps:

Step 1

First list all ordinary pay paid to the employee during the relevant pay period (this is the period in which you pay the employee their basic pay, ie, for a monthly-paid employee, the relevant period would be one month).

If your payroll provider can give you a report detailing an individual's "ordinary pay" for the purposes of GRG reporting this could considerably reduce the amount of administration associated with this step in your reporting obligations and this may be something to discuss with them.

Step 2

With regards to bonus pay, which is paid for a different period to the relevant pay period, divide the amount by the length of the bonus period and multiply by the length of the relevant pay period. This ensures that the bonus pay is pro-rated for the relevant pay period.

For these purposes, a year is treated as 365.25 days, and a month as 30.44 days.

Step 3

Take the amounts from Step 1 (as/if they have been adjusted by step 2) and add them together.

Step 4

Multiply the figure found from Step 3 by the ‘appropriate multiplier’ – this is 7 divided by the number of days in the relevant pay period (a month is 30.44 days and a year is 365.25).

If an employee is paid hourly, then this step is not normally required.

Step 5

Divide the final amount by the number of working hours in a week for that employee.

Employee A.

A's contract of employment provides for a 35-hour working week. A routinely works more than 35 hours a week but does not get paid any overtime. A's current annual salary is £25,000 and he is paid monthly.

Assuming A can be said to have "normal working hours", A's hourly rate of pay would be (£25,000 ÷ 12) x (7 ÷ 30.44) ÷ 35 = £13.69. If A cannot be said to have "normal working hours" then it would be necessary to work out the hourly rate using his average working hours over a 12-week period.

Employee B.

B is paid by the hour, with varying contractual rates of pay. B receives £6.70 an hour for daytime shifts, and £10 an hour for shifts carried out after 7 pm. B is paid weekly, according to her timesheet of hours worked. In the pay week including 5 April, B worked 25 hours at the daytime rate, and 10 hours at the additional rate.

B's hourly rate of pay is (25 x £6.70) + (10 x £10) ÷ 35 = £7.64.

Employee C.

C is on their maternity leave and is receiving statutory maternity pay of £139.58 a week. On 5 April, she receives a pro-rated discretionary annual bonus of £2,000, relating to the last financial year. Her contractual hours are 35 a week, and she is paid monthly.

C is not a full-pay relevant employee, because she is on her maternity leave, and so there is no need to calculate her hourly rate of pay for the purposes of gender pay gap reporting. However, her discretionary annual bonus would need to be reported as part of the gender bonus gap figures.

Where the employee has normal working hours that do notdiffer from week to week, the weekly working hours are the contractual hours.

Where the employee does not have normal working hours, or the number of normal working hours varies from week to week, the weekly working hours are calculated as the average number of working hours over a 12-week period, ending with the last complete week of the relevant pay period.

Once the hourly rates of pay have been fully calculated for all employees, you will need to present the overall gender pay gap figures by calculating both the mean and the median average hourly rates.

The following formula will be used to work out the GPG, where A is mean (or median) male pay, and B is mean (or median) female pay.

(A – B) x 100 = %

A

A negative pay gap figure would mean that the average pay of men is lower than the average pay of women.

The calculation of the gender bonus gap is fairly straightforward.

Using the same formula as for calculating the GPG, you can work out gender bonus gap, where A is mean bonus pay of all male relevant employees, and B is the mean bonus pay of all female relevant employees.

You will need to add together the different types of "bonus pay" that have been received during the 12-month period in order to calculate the average bonus pay. This could include sales commission, profit shares and productivity bonuses.

You are required to publish your GPG information on your company website, presented in a manner that is accessible to all employees and the public, and the information must be visible online for at least 3 years.

In addition, the government has set up a website where you will be required to upload your GPG data. You will need to accompany the GPG data to the government with a written statement that confirms that all the information is accurate. This written statement of accuracy must be signed by a senior individual of the organisation, such as a director or partner.

The UK Government has recently stated that although entirely voluntary, the provision of a contextual narrative alongside the GPG information will be strongly encouraged. It is foreseen that many employers will take the opportunity to provide some kind of narrative, in order to explain particular circumstances or anomalies that have led to a higher than expected GPG. For example, you may like to provide narrative explaining the degree to which overtime is routinely worked by employees and the proportion of women to men regularly working overtime. Depending on the gender split of these employees, this may have a hidden impact on your actual GPG.

Should you find that our figures do show a significant gender pay gap the narrative around this will be crucial to explain the factors that might underlie this and to avoid the impression that a genuine gender bias exists in the organisation.

Find it useful? Please share!

Find it useful? Please share!

Last updated: 08 July 2024 | © KIS Bridging Loans 2024 | Terms & Conditions